Research what actually works

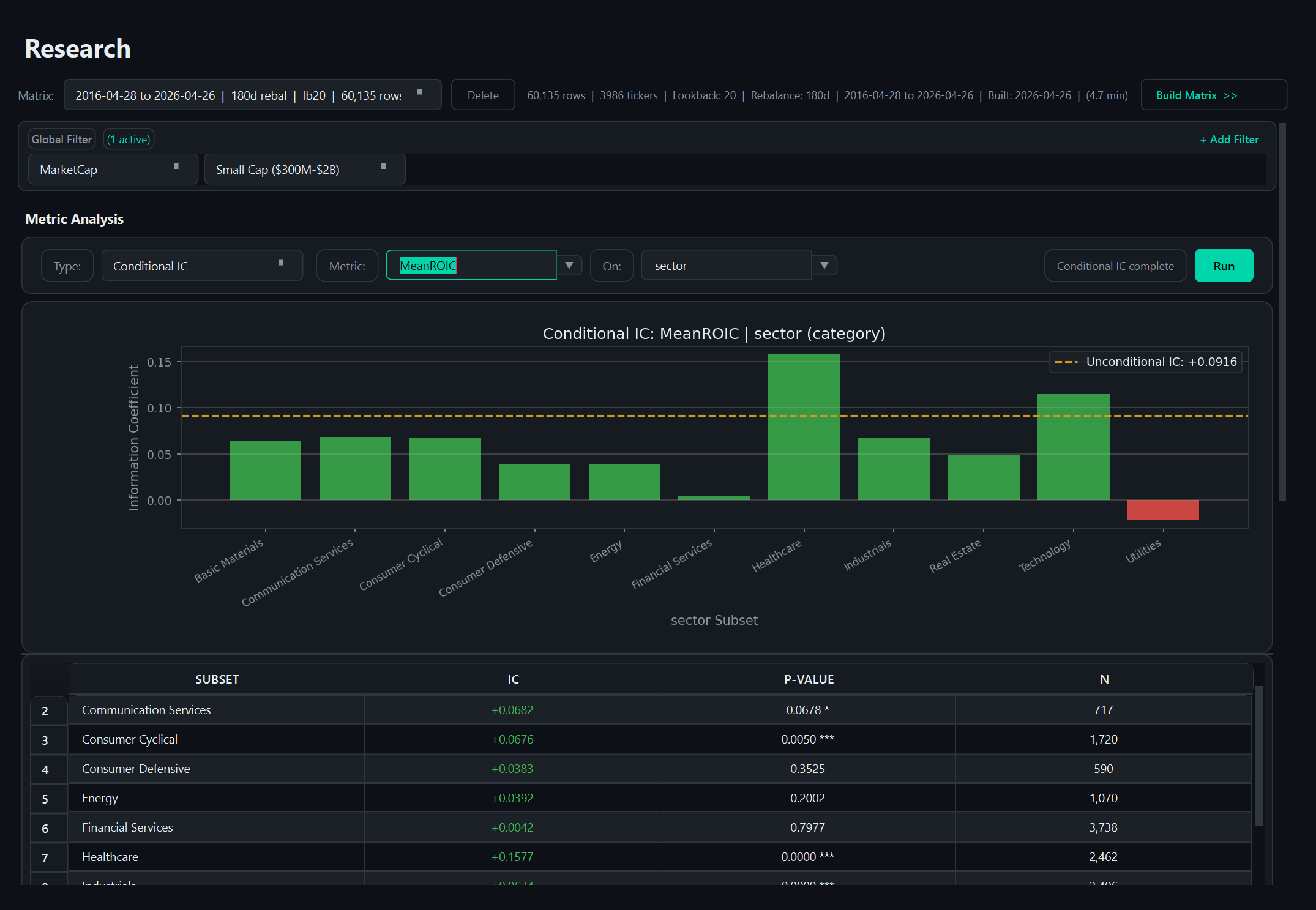

120+ financial metrics computed across 5,000+ US stocks, with signal rankings, quintile analysis, and threshold scanning. See which metrics have historically predicted returns instead of guessing.

Research what actually works, build multi-factor strategies as visual rules, backtest against 20 years of real history, and — when you're ready — automate the whole thing through Interactive Brokers. One desktop app, no code.

A complete workflow for systematic equity investing — each step grounded in real data, and each step transparent enough that you can defend its assumptions.

120+ financial metrics computed across 5,000+ US stocks, with signal rankings, quintile analysis, and threshold scanning. See which metrics have historically predicted returns instead of guessing.

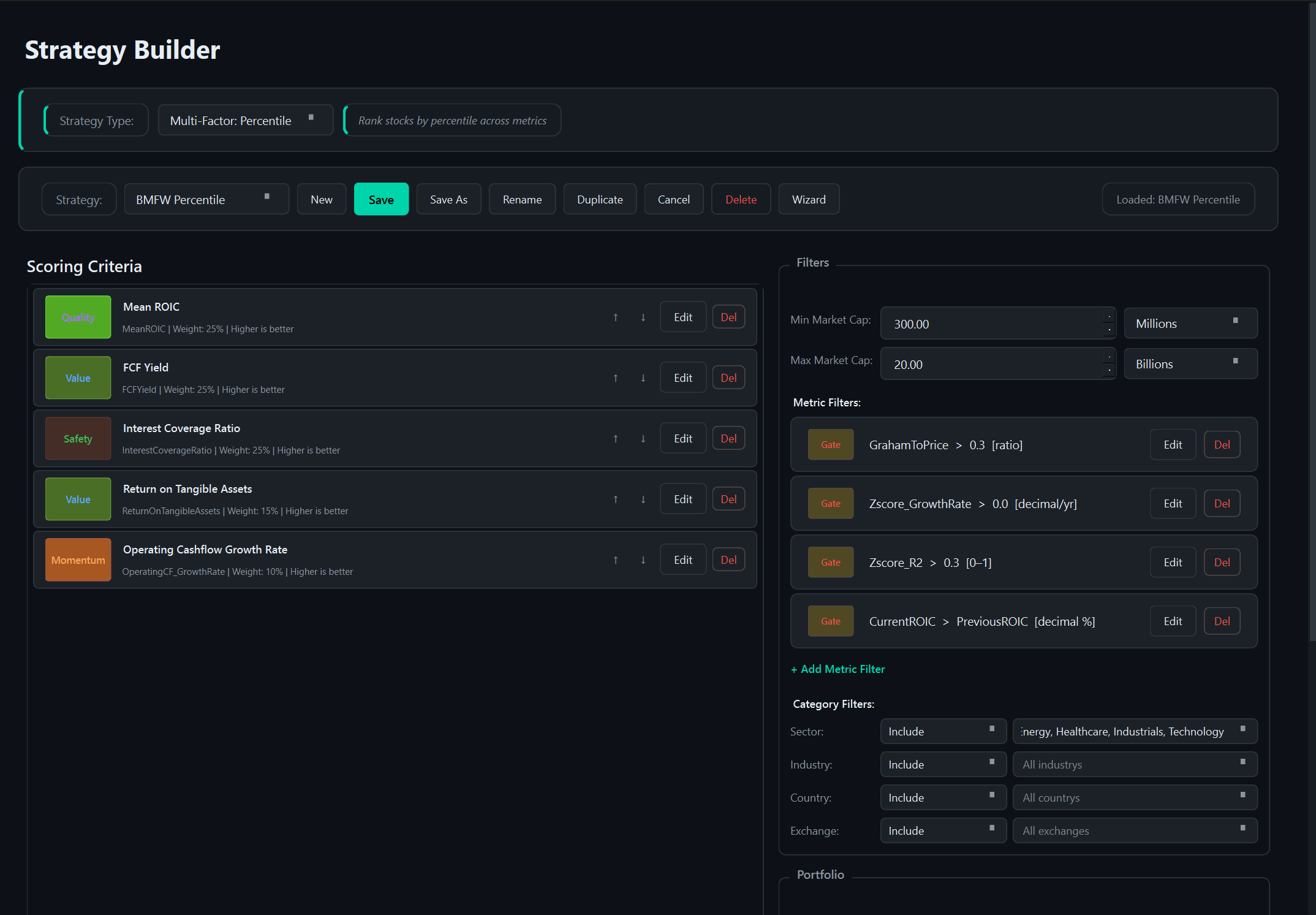

Compose multi-factor scoring strategies as cards. No code, just rules: free cash flow yield, return on capital, momentum, debt levels. Add filters for sector, market cap, country.

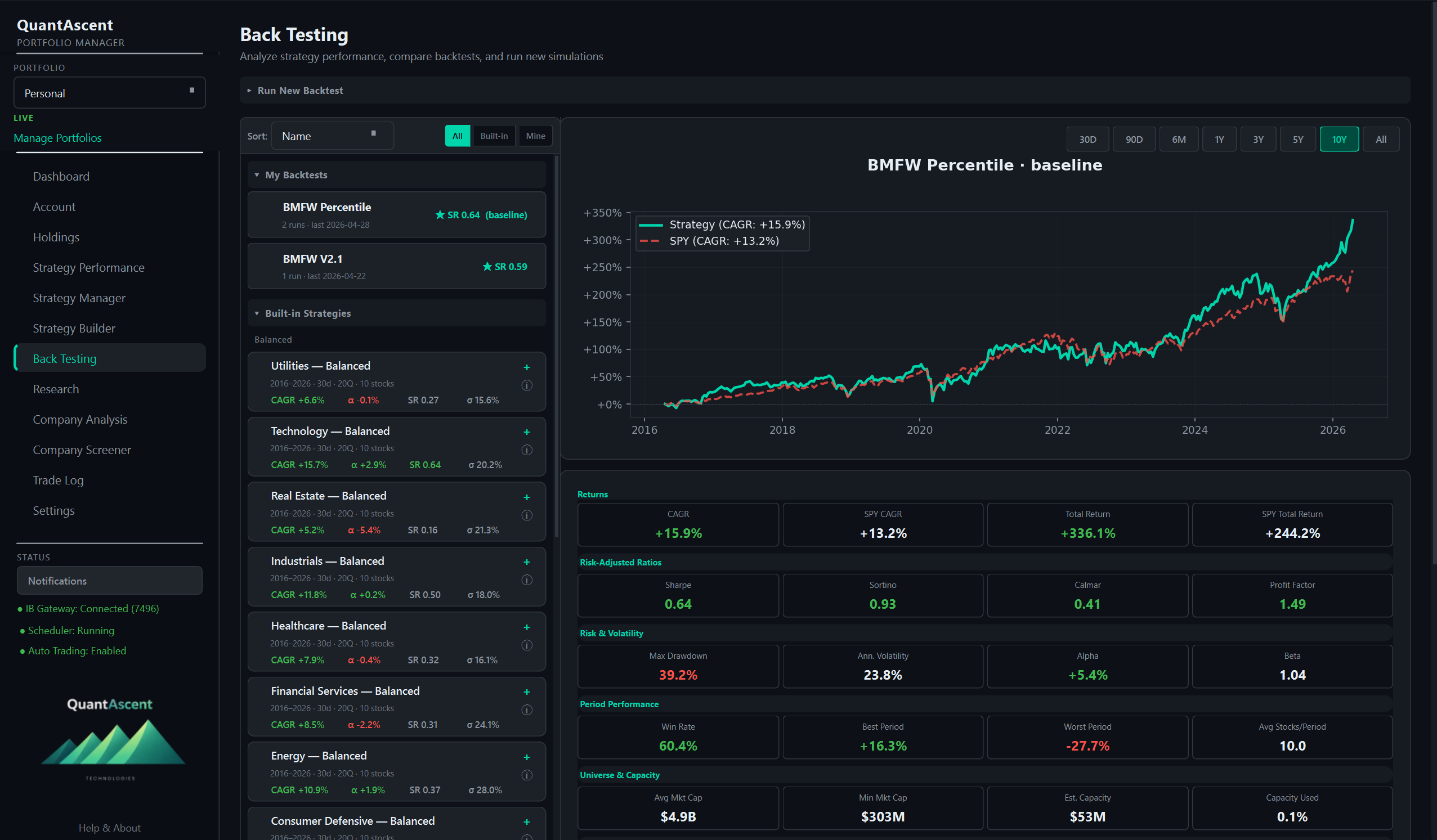

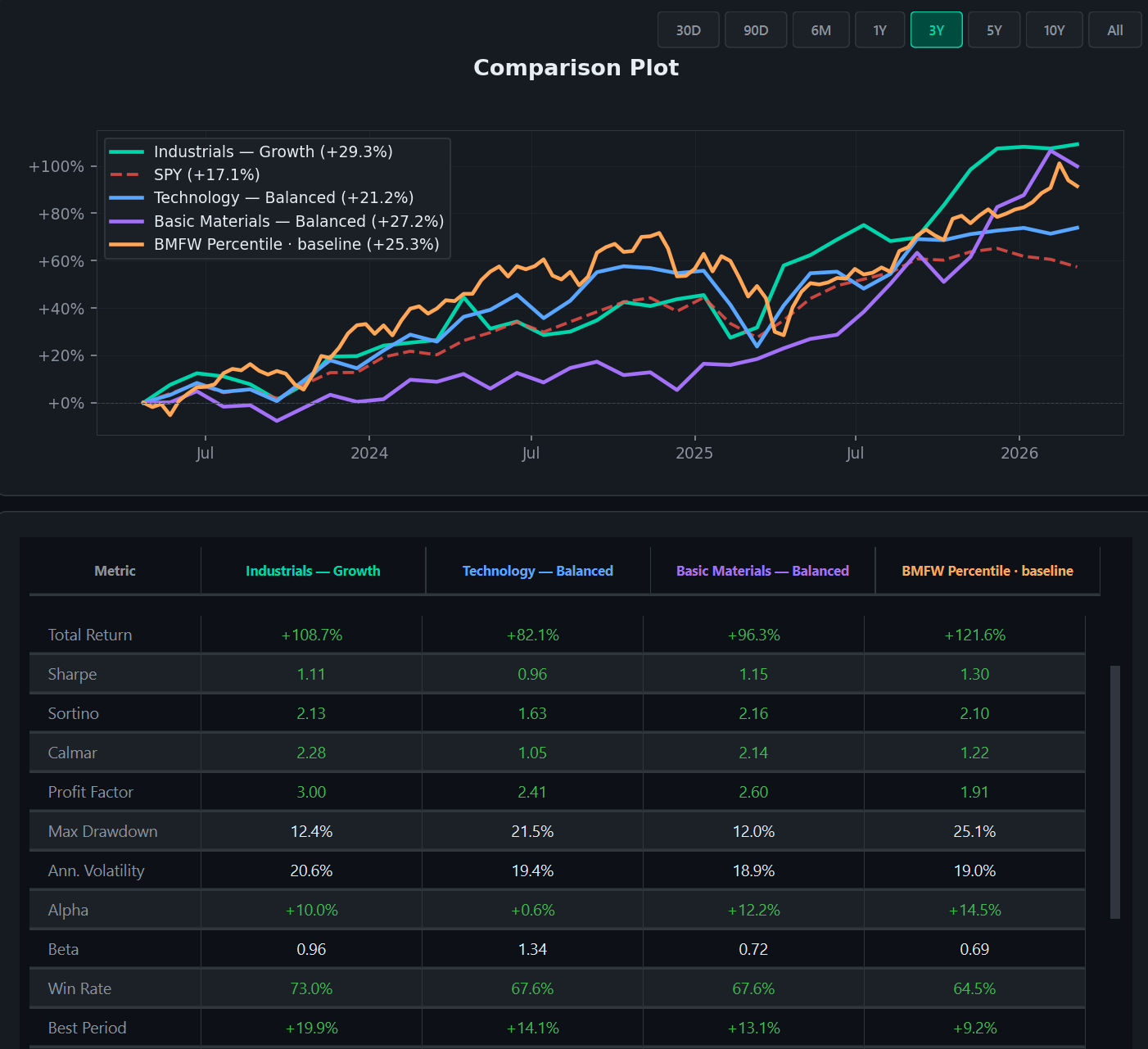

Run your strategy against real historical data. Get 16 performance metrics — Sharpe, Sortino, Calmar, alpha/beta, max drawdown, win rate — all benchmarked against the S&P 500.

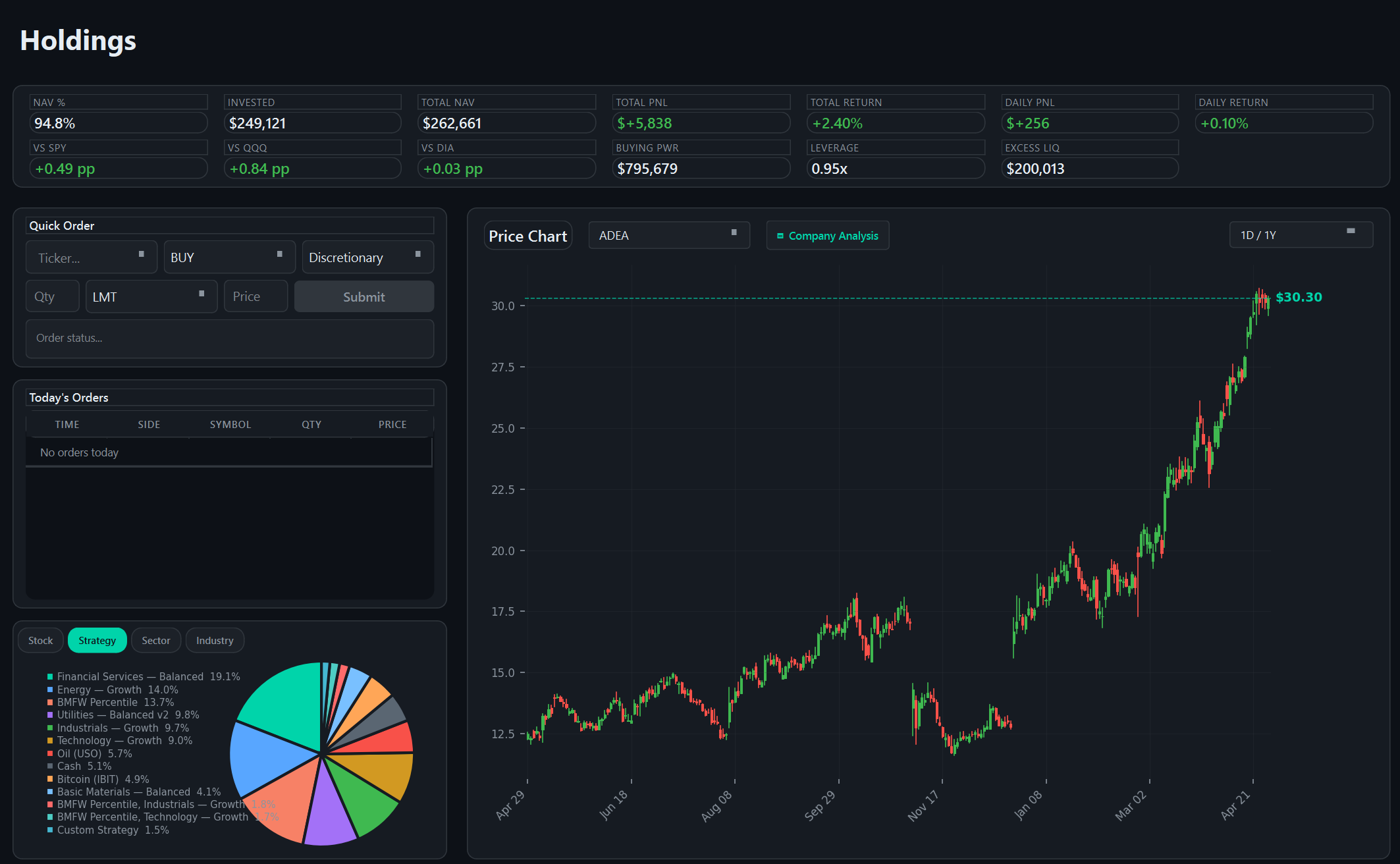

Connect Interactive Brokers for automated rebalancing. Every trade, lot, dividend, and tax event tracked automatically. See your real performance against the benchmark.

Three places you'll spend most of your time: the metric explorer, the strategy builder, and the backtest report.

Pick any of 120+ metrics, see how it has separated winners from losers across two decades, and decide whether it earns a place in your strategy. Quintile breakdowns, threshold scans, and signal rankings — all from real fundamental data.

Stack factor cards, weight them, layer filters. No code, just rules. Save versions as you iterate, branch when you want to test variants, and pick which one to backtest next.

16 metrics — Sharpe, Sortino, Calmar, alpha, beta, max drawdown, win rate, and more. Every backtest benchmarked against the S&P 500 and saved automatically so you can compare runs side-by-side.

Live positions, lots, dividends, and tax events — straight from your Interactive Brokers account. P&L tracked by strategy, by lot, by realized vs. unrealized, with tax schedules built in.

QuantAscent is in closed alpha — access is by approval only and signing up doesn't guarantee admittance. Use the form below to share your background, ask about the platform, or check on an application. We reply within 1–2 business days.

If you don't hear back by then, check spam and then drop a line to [email protected].